SAN ANTONIO — What’s your retirement number? $1 million, $2 million, maybe $3 million? Here are the key steps to take in order to reach your goal, no matter what dollar amount you're envisioning.

Your golden years are supposed to be one of the most relaxing times of your life. If you want to live comfortably while financially secure, you need to have a plan.

Karl Eggerss, principal and financial advisor at CAPTRUST, says you should determine your target and then work your way backwards. He says think about major expenses like upcoming weddings, vacations and college tuition.

“Factor all of that into a plan so you can figure out: What is it going to take? How much do I have to save and earn to get to a number that’s going to sustain that lifestyle and all those expenses for the rest of my life?” said Eggerss. “Is $1 million what it used to be? We know because of inflation it’s not. $1 million doesn’t go as far today as it did 20 years, 30 years ago.”

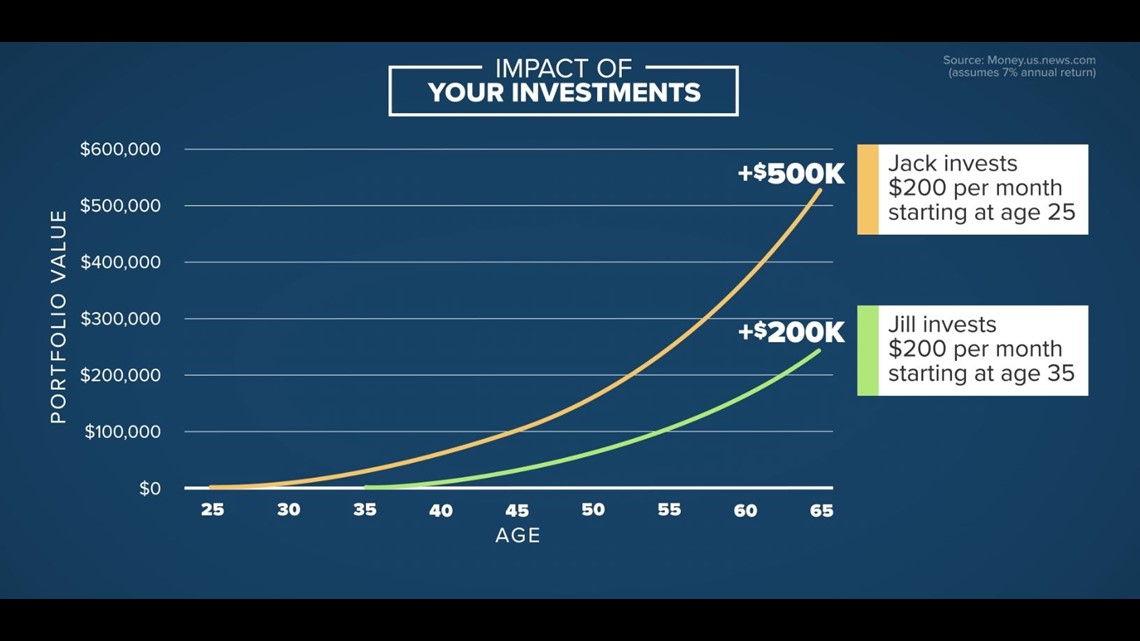

In order to pull off the retirement of your dreams, focus on the power of compounding. KENS 5 has a fictitious example (labeled #1) to illustrate the impact of investments over time.

Jack stayed focused and invested $200 per month, starting at age 25. Jill, who partied a little too hard, started a decade later than Jack, investing the same amount per month.

When they both hit age 65, Jack ended up with more than $500,000. Jill had saved more than $200,000.

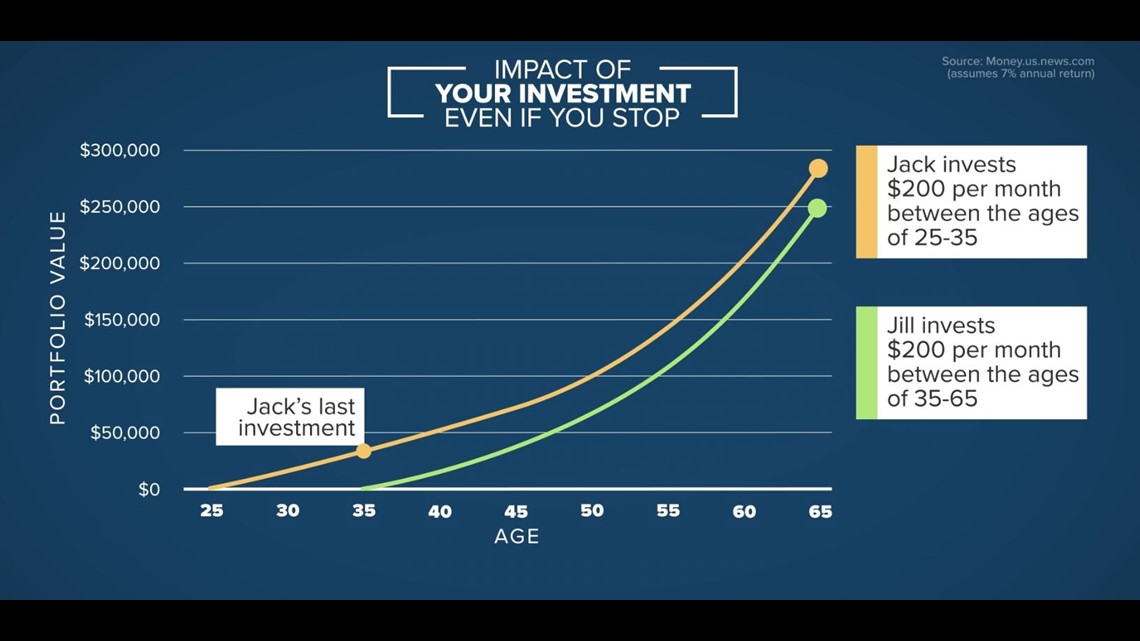

In another situation (labeled example #2 above), Jack saved $200 worth of investments every month starting at age 25. Jill did the same, but started a decade later at age 35. Even if Jack stopped contributing after 10 years, he would still have more than she would by retirement age.

“Don’t always live up to what your income is. If you live beneath your means and below your means, you will tend to have more cash flow, and tend to have more savings in the future,” said Eggerss. “Long-term stocks do a great job of compounding wealth. Diversifying and not taking excessive risk in one or two companies is typically, the way most people will accomplish their financial goals.”

Eggerss added that one of the biggest mistakes people make is assuming their expenses today will be the same decades later. He says another mistake is when people take financial advice from family or friends.

Instead, he recommends seeking a trusted financial professional.